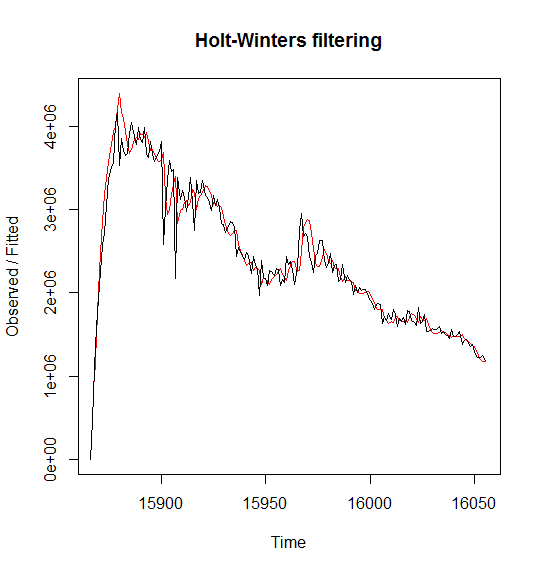

2 мӢңм°ЁмғҒкҙҖ(м„ н–ү, нӣ„н–ү) #

> tmp

curr_val prev_val

5 3949515 4316313

6 3835690 4149917

7 3975137 4165120

8 3993659 4050347

9 3942373 3949515

10 3825807 3835690

11 3920338 3975137

12 3586568 3993659

13 3633877 3942373

14 3444306 3825807

15 3903889 3920338

16 3529384 3586568

17 3531147 3633877

18 3518490 3444306

19 3481886 3903889

20 3298512 3529384

21 3400325 3531147

22 3641914 3518490

23 3466527 3481886

24 6028886 3298512

25 6543880 3400325

26 5516709 3641914

27 5100715 3466527

28 5259752 6028886

29 5370662 6543880

30 5009019 5516709

31 4778911 5100715

32 4836214 5259752

33 4662136 5370662

tmp <- na.omit(tmp)

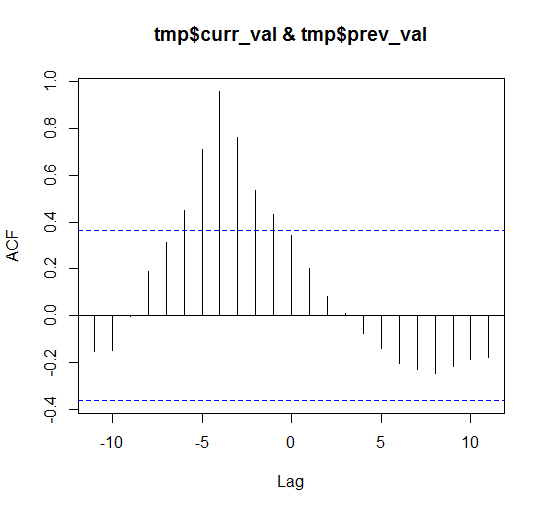

ccf(tmp$curr_val, tmp$prev_val)

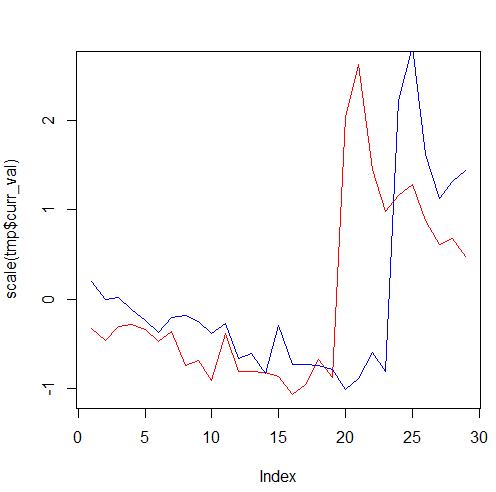

мІ« лІҲм§ё л§Өк°ңліҖмҲҳлҘј кё°мӨҖмңјлЎң м–јл§ҲлӮҳ м„ н–ү/нӣ„н–ү н•ҳлҠ”м§Җ м•Ң мҲҳ мһҲлӢӨ. к°ҖмһҘ ліјлЎқн•ҳкІҢ лӮҳмҳЁ л¶Җ분мқҙ x축м—җ -4 мқҙлӢҲк№Ң tmp$curr_valк°Җ лҢҖлһө 4мқјм •лҸ„ л№ лҘҙлӢӨ.

мІ« лІҲм§ё л§Өк°ңліҖмҲҳлҘј кё°мӨҖмңјлЎң м–јл§ҲлӮҳ м„ н–үн•ҳлҠ”м§Җ м•Ң мҲҳ мһҲлӢӨ.

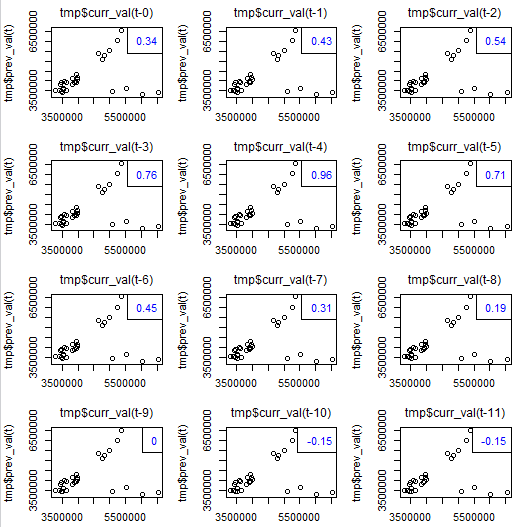

lag.plot2(

itall.R

itall.R) н•ЁмҲҳлҘј мқҙмҡ©н•ҙм„ң м°ЁнҠёлҘј к·ёл Өліҙмһҗ.

source("http://databaser.net/moniwiki/pds/TimeSeries/itall.R")

lag.plot2(tmp$curr_val , tmp$prev_val, 11)

н‘ңмӨҖнҷ”н•ҙм„ң лқјмқё м°ЁнҠёлҘј к·ёл Өліҙмһҗ.

plot(scale(tmp$curr_val), type="l", col="red")

lines(scale(tmp$prev_val), col="blue")

мөңлҢҖ/мөңмҶҢ көҗм°ЁмғҒкҙҖ л°Ҹ мӢңм°Ё (

![[http]](/moniwiki/imgs/http.png) м¶ңмІҳ(http://blog.naver.com/lofie21?Redirect=Log&logNo=110171809189)

м¶ңмІҳ(http://blog.naver.com/lofie21?Redirect=Log&logNo=110171809189))

max_ccf <- function(...)

{

d <- ccf(...)

cor <- d$acf[,,1]

lag <- d$lag[,,1]

dd <- data.frame(cor, lag)

max_val <- dd[which.max(dd$cor),]

min_val <- dd[which.min(dd$cor),]

result <- c()

if(abs(max_val[1]) >= abs(min_val[1])){

result <- max_val

} else {

result <- min_val

}

return(result)

}

max_ccf <- function(...)

{

d <- ccf(...)

cor <- d$acf[,,1]

lag <- d$lag[,,1]

df <- data.frame(cor, lag)

max_val <- df[which.max(df$cor),]

return(max_val)

}

min_ccf <- function(...)

{

d <- ccf(...)

cor <- d$acf[,,1]

lag <- d$lag[,,1]

df <- data.frame(cor, lag)

min_ccf <- df[which.min(df$cor),]

return(min_ccf)

}

мҳҲлҘј л“Өм–ҙ, лӢӨмқҢкіј к°ҷмқҙ кІ°кіјк°Җ лӮҳмҷ”лӢӨл©ҙ..

> max_ccf(sales, val)

cor lag

12 0.8932095 -1

- мөңлҢҖ мғҒкҙҖ кі„мҲҳлҠ” 0.89

- мӢң간축 мғҒм—җм„ң salesк°Җ valліҙлӢӨ -1мқј л’Өм ё мһҲмқҢмқ„ лң»н•Ё.

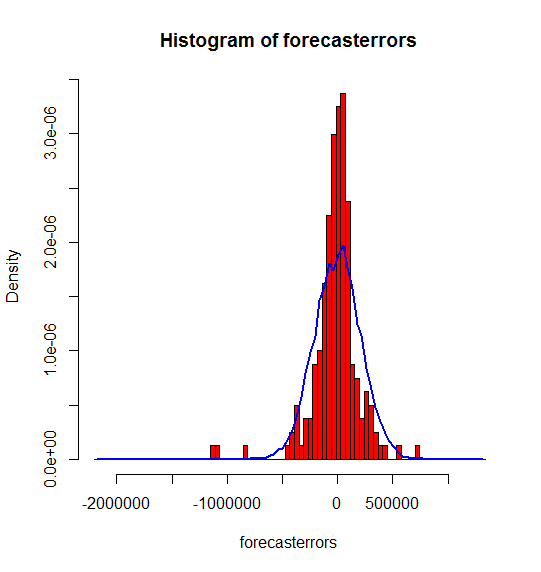

3 plotForecastErrors #

plotForecastErrors <- function(forecasterrors)

{

# make a histogram of the forecast errors:

mybinsize <- IQR(forecasterrors)/4

mysd <- sd(forecasterrors)

mymin <- min(forecasterrors) - mysd*5

mymax <- max(forecasterrors) + mysd*3

# generate normally distributed data with mean 0 and standard deviation mysd

mynorm <- rnorm(10000, mean=0, sd=mysd)

mymin2 <- min(mynorm)

mymax2 <- max(mynorm)

if (mymin2 < mymin) { mymin <- mymin2 }

if (mymax2 > mymax) { mymax <- mymax2 }

# make a red histogram of the forecast errors, with the normally distributed data overlaid:

mybins <- seq(mymin, mymax, mybinsize)

hist(forecasterrors, col="red", freq=FALSE, breaks=mybins)

# freq=FALSE ensures the area under the histogram = 1

# generate normally distributed data with mean 0 and standard deviation mysd

myhist <- hist(mynorm, plot=FALSE, breaks=mybins)

# plot the normal curve as a blue line on top of the histogram of forecast errors:

points(myhist$mids, myhist$density, type="l", col="blue", lwd=2)

}

p10 <- forecast(m, 10)

plotForecastErrors(p10 $residuals)

8 нҸүнҷң #

library("forecast")

data(gold)

g <- data.frame(g = na.omit(coredata(gold)))$g

y_width <- c(min(g) - min(g) * 0.05, max(g) - max(g) * 0.05)

plot(g, type="l", lty="dotted", ylim=y_width)

par(new=T)

plot(smooth(g, twiceit=T), type="l", col="blue", ylim=y_width, ylab="")

мқҙлҸҷмӨ‘к°„к°’ н•ЁмҲҳ : runmde()